Being able to buy your own home is the Filipino dream. Whatever your motivations are, the only way for first-time homebuyers is to move forward until you sign on the dotted line and receive the keys.

However, having your own space you can call home, even if it is a rental, may suit you just fine. Buying your own house may not always be the way to go — at least not just yet — especially if you’re always on the go or require flexibility.

I, for one, personally know of a couple who has moved to different home rentals 40 times already (along with their four kids!) and has never once considered investing in a condo, townhouse, or house and lot to live in permanently yet.

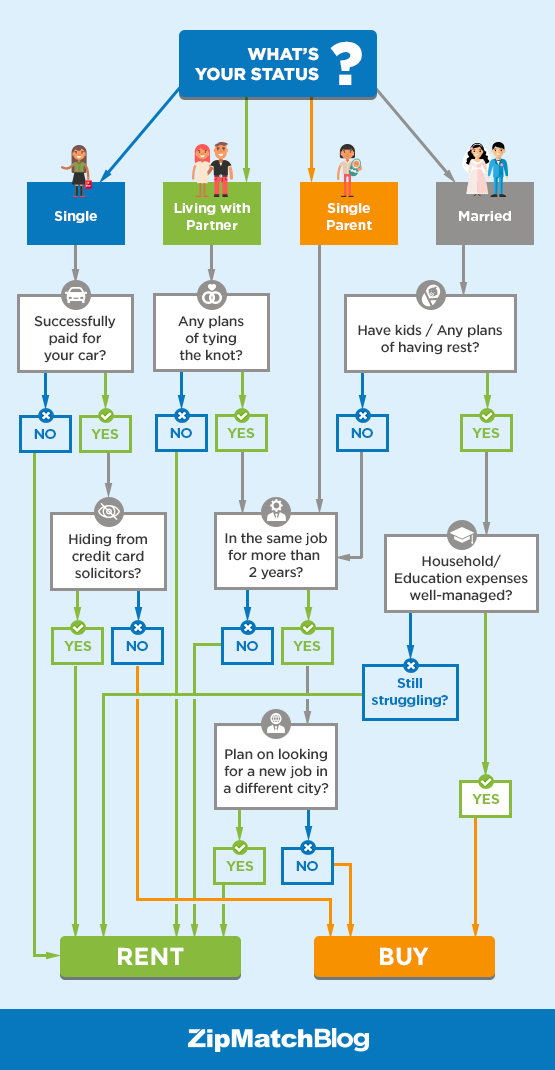

So how do you know really when you’re ready to buy or rent? We’ve created a roadmap to help you mull things over and make a home decision that you’re definitely going to be comfortable with.

What kind of lifestyle do you aspire to have?

Every person has his or her own preference when it comes to choosing their next home. But lifestyle can be a key factor in determining the level of commitment you can make in your next home.

If you’re not fond of sticking to one place for a long time for whatever your reason is (work, school, business, or travel plans), an apartment, condo or townhouse for rent may be the path for you now.

Renting offers you more mobility and flexibility, especially if you do not plan on spending more money on a home in the next five years or so.

Meanwhile, if the time comes that you already want to settle in your own home, you may want to consider investing in your rental home, or in a new property but in the same neighborhood. You probably have (or would like to have) a firsthand experience of how it is to live in the area, and buying a property there to live in permanently would be the next logical real estate decision to do.

What does your emergency fund look like?

An emergency fund is basically a special fund that can cover up to 6 months’ worth of household expenses or a particularly large, immediate expense.

People who are eyeing to settle in their own homes have built an emergency fund as a form of insurance in case they couldn’t keep up with the amortization payments well after they have signed the dotted line. The emergency fund will help them make sure that they pay on time and without delay, and avoid the risk of getting their loan defaulted and put their home up for foreclosure.

If you have yet to build an emergency fund, it would be best to stick with a rental for the meantime. If you’re eyeing to own a home in the future, though, you can come up with (or reschedule) your homebuying savings timeline and attempt to achieve every financial amount milestone towards your emergency fund goal. If you have another financial goal in mind that you’d like to hit first, like owning a car, a travel fund for a trip abroad, or even tuition for a post-graduate diploma, it’s your call if you like to either make the adjustments or a little sacrifice.

Can you keep up with monthly home loan payments at a slightly higher rate?

Rental payments are often stable, and will only change the slightest if there is a major economic event (ex. inflation) or an upgrade on the building your unit is located (ex. newly-installed elevator). For people who are still managing their debt and other financial responsibilities, or would like to have a little bit of freedom with their money, living in a rental is financially convenient.

If you have manageable to no debt and would like to build equity for your future, then it only takes dedication to buy and keep your own home.

Unlike rental payments, amortization payments tend to be a little more expensive during the first few years. This is computed so you can pay off the interest early, and focus on the principal amount later. On top of that, you will be paying off periodic costs such as property taxes and insurance, and unexpected expenses like maintenance and capital expenses (potential expenses that would add market value to your property).

Are you gearing for a huge life change?

A life change will have a huge impact in the kind of living situation you need. Whether you’re in a new city for work purposes, planning to leave work for a better opportunity, get married or grow a family, a life change is one factor that will help you decide the kind of home you’ll need.

Moreover, a life change can be costly. Say you need to move into a new city for work in the next three years. Unless you plan to be in the landlord business, you may want to stick with a rental and recoup the deposit should you decide to move out soon.

But if you are planning to make your current city your home in the next five years, or look for a home for your growing family to establish roots, then investing in a permanent home makes sense.

Still not sure whether you’d rent or buy? Mull it over by checking out your next home here.